How We Calculated Homeowners Insurance Ratings

Home insurance premiums aren’t just climbing — they’re spiking in 2025. According to the U.S. Bureau of Labor Statistics, the national producer price index (which measures the average change in producers’ prices over time) for homeowners insurance jumped by almost 9% between April 2024 and April 2025. In this article, the MarketWatch Guides team breaks down what you can expect to pay for home insurance this year and what you can do to keep costs in check.

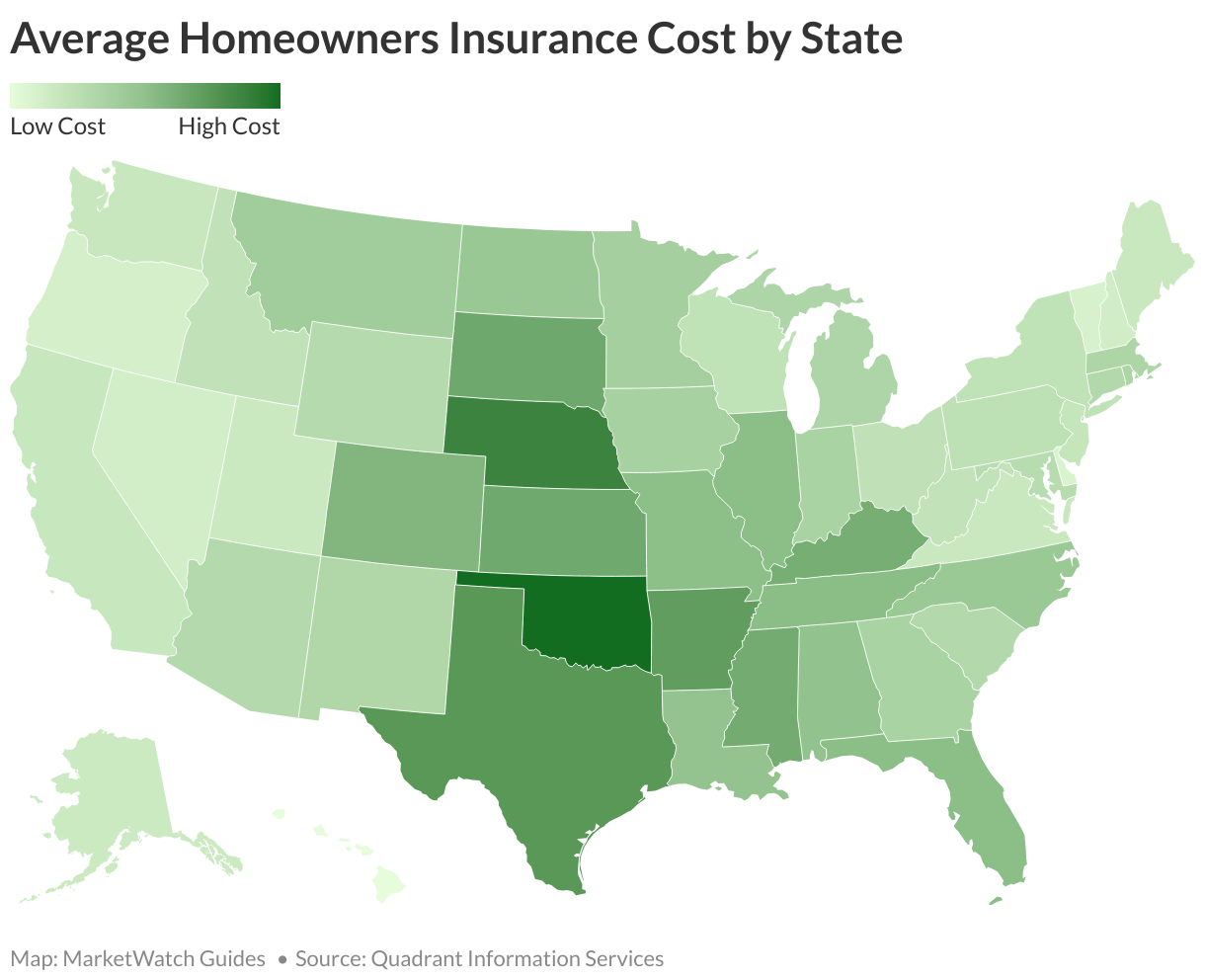

Home Insurance Cost by State

Because of local risk factors, the average cost of home insurance in your state can differ significantly from the national average. Whether you live somewhere with an elevated crime rate, a higher risk for extreme weather or an unusually cheap cost of living, state averages range from $71 to $529 per month.

For instance, Oklahoma, Nebraska and Texas are the most expensive states for homeowners insurance due to the significant risk of severe weather such as tornadoes, hurricanes and strong storms. On the other hand, Delaware, Hawaii and Vermont are the most affordable states for a policy, which could be because they typically have less exposure to major natural disasters.

Use the map below to find out the average rate the typical resident of your state pays for home insurance.

The Top Home Insurance Companies by State

Home Insurance Cost by City

Although the average home insurance costs by state can help you get an overview of rates, cities face more specific risks that can affect local rates. To help you get a more accurate estimate, we compiled costs in over 12,000 cities using data from over 15,000 ZIP codes. You can look up your city’s average rates using the search field in the table below.

Home Insurance Cost by Provider

In addition to location, the provider and dwelling coverage limits you select can significantly impact your homeowners insurance rates. Dwelling coverage determines the amount your insurer will pay to repair your property after a covered loss. Many providers require you to insure your property for 80% to 100% of its replacement cost.

Below are some of our top home insurance companies and their average monthly premiums for various dwelling coverage amounts.

| Provider | $250,000 | $350,000 | $450,000 | $750,000 | $1 million |

|---|---|---|---|---|---|

| AIG Insurance | $83 | $105 | $129 | $206 | $258 |

| Allstate | $191 | $230 | $273 | $387 | $478 |

| American Family Insurance | $259 | $315 | $347 | $413 | $467 |

| American Select Insurance | $192 | $224 | $256 | $360 | $439 |

| Amica | $126 | $165 | $198 | $293 | $370 |

| Armed Forces Insurance | $152 | $182 | $213 | $305 | $361 |

| Auto-Owners Insurance | $176 | $216 | $254 | $357 | $454 |

| Chubb | $178 | $222 | $265 | $403 | $499 |

| Country Mutual Insurance | $206 | $259 | $320 | $484 | $617 |

| Erie Insurance | $169 | $218 | $264 | $397 | $476 |

| Farmers | $185 | $246 | $306 | $411 | $489 |

| Island Insurance Co. | $56 | $80 | $104 | $178 | $238 |

| Kemper Insurance | $228 | $255 | $286 | $400 | $531 |

| Nationwide | $196 | $248 | $303 | $434 | $512 |

| Progressive | $211 | $238 | $268 | $369 | $445 |

| State Farm | $162 | $197 | $234 | $336 | $403 |

| The Hanover | $273 | $342 | $389 | $537 | $613 |

| Tokio Marine Insurance | $66 | $93 | $121 | $230 | $319 |

| Travelers | $394 | $380 | $374 | $368 | $423 |

| Umialik Insurance Co. | $74 | $95 | $121 | $187 | $246 |

| Union Mutual | $72 | $90 | $111 | $174 | $232 |

| USAA | $160 | $199 | $234 | $312 | $362 |

Factors That Impact Home Insurance Rates

Your state, your city and even your neighborhood can affect your home insurance premium. However, location is just one of many factors that can account for how risky insurers think it is to sell you coverage. In this section, we’ll look at other important variables insurers consider when determining your rates. Unless stated otherwise, the tables below are for a $350,000 dwelling with a $1,000 deductible.

Claims History

When you file a claim for a covered loss, your insurance company could pay for most or all of the damages. However, filing that claim will likely increase your rates when you renew your policy. Even if you switch companies, most insurers review the past five to seven years of your claims history with previous providers and charge higher rates if you filed a claim within that time frame.

The table below shows the three most common types of claims and the average monthly premium, cheapest national provider and cheapest provider rates for each type.

| Claim Type | Average Monthly Premium | Cheapest Provider | Cheapest Provider’s Average Monthly Premium |

|---|---|---|---|

| Wind and hail | $240 | USAA | $202 |

| Fire and lightning | $262 | State Farm | $212 |

| Water damage and freezing | $259 | State Farm | $212 |

Credit Score

In most states, insurance companies will check your credit score to calculate your relative risk for filing claims. Some states — such as California, Hawaii, Massachusetts and Michigan — don’t allow insurers to use credit scores for home and auto insurance rates, meaning your score shouldn't affect your rates in one of those states.

The table below shows how the national average home insurance premium and the cheapest national provider change based on credit score.

| Credit Tier | Average Monthly Premium | Cheapest Provider | Cheapest Provider’s Average Monthly Premium |

|---|---|---|---|

| Poor | $386 | Armed Forces Insurance | $300 |

| Good | $244 | Armed Forces Insurance | $182 |

| Excellent | $194 | Auto-Owners Insurance | $121 |

Dwelling Age

Older dwellings are more likely to experience issues than newer homes. This is because of the accumulated wear and tear on a home’s infrastructure, foundation, plumbing, electrical system and other major systems. Sometimes, repairing age-related problems can become complicated and expensive. Often, you must improve outdated structures and systems and update to modern building codes. Insurance companies equate older homes with an increased risk of filing a claim and price your coverage accordingly.

A home's roof is one of the biggest concerns, since it's the first line of defense against weather events such as hailstorms, windstorms and severe rainstorms. You’ll find lower home insurance premiums if you have a newer roof. Some insurers won’t offer coverage for a roof that’s more than 20 years old.

The table below shows how premiums can change based on a home’s age.

| Home Age | Average Monthly Premium | Cheapest Provider | Cheapest Provider’s Average Monthly Premium |

|---|---|---|---|

| 2024 | $134 | Progressive | $87 |

| 1980 | $210 | State Farm | $186 |

| 1950 | $209 | USAA | $179 |

Insurance Deductible

Most home insurance policies have a deductible, which is the portion of covered losses that the policyholder is responsible for paying before policy benefits kick in. Choosing a higher deductible reduces your premiums, but it increases your out-of-pocket costs if damages occur. Having a lower deductible increases your premiums but minimizes your out-of-pocket costs during a loss.

The table below shows how average homeowners insurance premiums can vary based on a home’s value and the deductible.

| Home Value | Average Monthly Premium With $500 Deductible | Average Monthly Premium With $1,000 Deductible | Average Monthly Premium With $5,000 Deductible |

|---|---|---|---|

| $250,000 | $206 | $200 | $158 |

| $350,000 | $248 | $244 | $199 |

| $450,000 | $288 | $279 | $233 |

| $750,000 | $387 | $377 | $326 |

| $1 million | $453 | $447 | $394 |

How To Save Money on Homeowners Insurance

While you’ll have little control over some factors, such as your home’s location or age, there are other ways to save money on home insurance premiums.

“By focusing on areas such as deductible amounts and liability limits while keeping a detailed inventory list, these changes can provide substantial savings each year while still protecting yourself against potential financial losses because of unforeseen events beyond one’s control.”

Bundle Policies

One of the best ways to save money on your homeowners insurance policy is to bundle your policy with another type from the same provider, typically car insurance. Bundling can save you anywhere from 5% to 25% on your premiums.

Look for Discounts

Many providers offer discounts for outfitting your home with a security system, enrolling in automatic payments or paying your bill in full and on time.

Make Renovations

Although home renovations can have significant up-front costs, insurers may see an updated and repaired home as a lower risk and might offer cheaper premiums. But if your home has an older roof or outdated systems, you might pay more for coverage.

Maintain Good Credit

By maintaining good credit or improving it, you may get lower home insurance premiums when you renew your policy.

Avoid Small Claims

Filing a home insurance claim, even a small one, is likely to increase your home insurance premiums when it’s time to renew your policy. Consider whether reporting a claim is worth this uptick in cost. For example, if you’ve filed a claim within the last few years or find that paying for a covered loss yourself will cost less than your deductible, you may not want to alert your home insurance provider.

Compare Providers

Not all home insurers calculate risk the same way. If you’re about to buy homeowners insurance or already have a policy and want to save money, we recommend getting quotes from several providers to compare prices. Also compare coverage options, customer reviews and third-party ratings.

Frequently Asked Questions About the Cost of Homeowners Insurance

Home insurance rates are going up because of increasing construction and repair costs, more extreme weather events and inflation, among other reasons. According to the Insurance Information Institute, home replacement costs increased 55% between 2020 and 2022. Rising costs for building materials and labor have increased the price of replacing or repairing your property, which affects your insurance premiums.

Also, multiple insurers have stopped selling homeowners insurance policies in high-risk states such as California and Florida, contributing to higher costs. For instance, insurers such as State Farm and Allstate stopped offering policies in California in 2023 because of a significant increase in construction costs, severe weather events and challenges in the state’s reinsurance market (though they may re-enter the market if some reinsurance issues are resolved).

No, house insurance isn’t cheaper without a mortgage. Your home is vulnerable to the same risks whether you own it outright or are still making payments, so home insurance providers don’t consider your mortgage status during underwriting.

Armed Forces Insurance has the cheapest homeowners insurance by dwelling cost on average, according to Quadrant Information Services.

According to cost data provided by Quadrant Information Services, the most expensive states for home insurance are:

- Oklahoma: $529 per month on average

- Nebraska: $467 per month on average

- Texas: $409 per month on average

- Arkansas: $396 per month on average

- South Dakota: $366 per month on average

Homeowners insurance typically doesn’t cover flooding or earthquake damage. Flood insurance and earthquake insurance are normally separate policies you may be able to add as endorsements, depending on your insurer. You can buy flood insurance from the federally backed National Flood Insurance Program or through some private insurers. In California, you can buy earthquake insurance from the California Earthquake Authority, a specialty insurer.

How We Gather Cost Data

Sources:

- U.S. Bureau of Labor Statistics, Producer Price Index - Insurance

*Data accurate at time of publication.